As the world becomes more digital, there are new ways for people to create a cryptocurrency. You can do this in three significant ways:

- Through Blockchain technology like Bitcoin or Ethereum

- By creating non-crypto currencies (such as fiat money) which act similarly but have less value than cryptocurrencies since they’re not necessarily tied directly into any cryptocurrency network)

- By minting your very own coin on an existing platform – such as Steemit, where anyone who creates content will earn some form of reward if other users upvote it!

This article will walk you through technical and business aspects, so please read it carefully before deciding what type of coin or token is best for your needs.

Learn more: How to secure your code with blockchain technology?

What is a Cryptocurrency?

You’ve probably heard of cryptocurrency and want to learn more about them.

Cryptocurrency is a type of digital currency that uses cryptography (a system for secure communication) in order, unlike fiat currencies such as dollars or euros; they’re decentralized! This means no central authority makes decisions about how money is created/printed.

Cryptocurrency is a decentralized digital currency that uses encryption techniques to regulate currency unit generation and verify fund transfers. Its main characteristics include anonymity, decentralization, and security. There is no centralized authority, government, or bank that regulates or tracks cryptocurrency.

There are currently hundreds of them worldwide. Cryptocurrencies come in many different forms, such as Bitcoin, which can be used at online or offline stores to buy goods from websites like Overstock (OSTK) without relying on a third party like Paypal (PYPL).

Even though virtual money has been available for a long time, Bitcoin is the most well-known and successful cryptocurrency, commanding the top spot in the cryptocurrency market. Today, over 1,600 different types of cryptocurrencies are available, and the number is still growing.

All of the information presented above makes companies see the benefits of Blockchain and consider creating a cryptocurrency. (Blockchain, a decentralized peer-to-peer (P2P) network made up of data blocks, is an essential cryptocurrency component. These blocks store transaction information in chronological order and follow a protocol for inter-node communication and validating new blocks. You cannot change the data stored in blocks without affecting all subsequent blocks).

Want to know more about Blockchain and what the future entails for this technology?

>> Read our article: Why is the world go crazy with Blockchain?

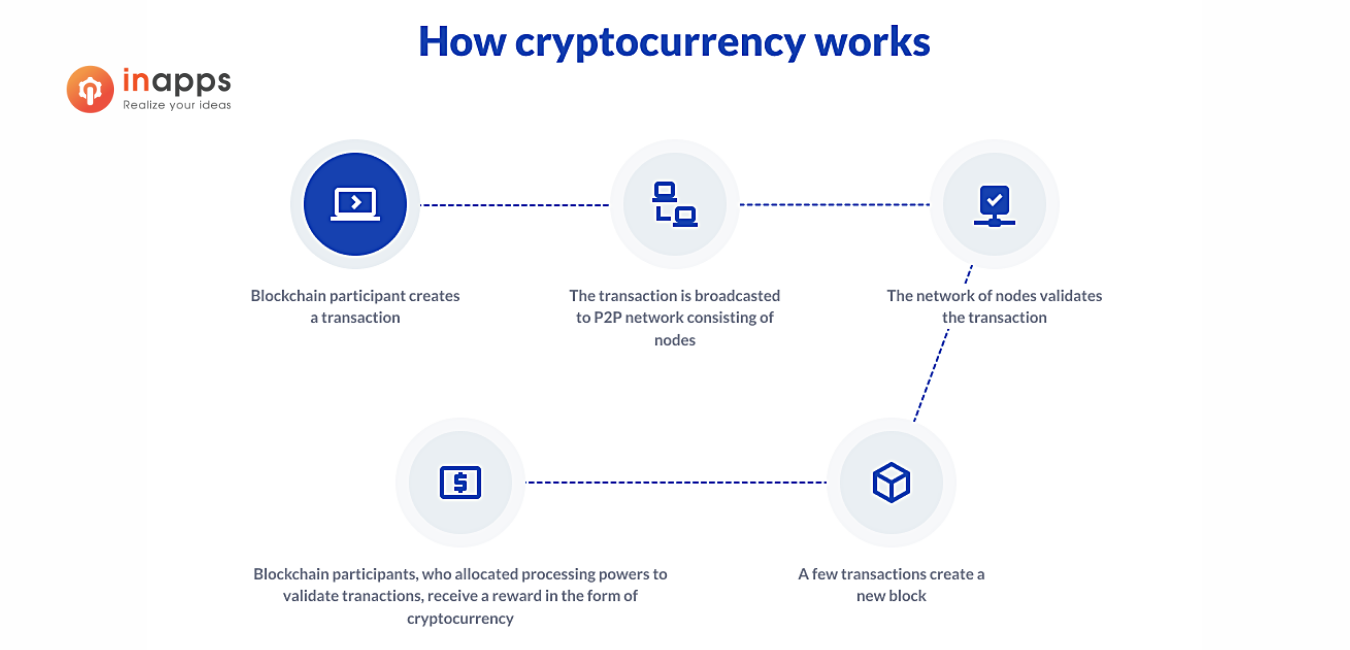

How Does a Cryptocurrency Work?

As previously mentioned, cryptocurrency is an essential component of the Blockchain. The consensus algorithms that govern the creation of new blocks are the foundation of distributed ledger technology. For a block to be registered in the Blockchain, it must be accepted by all participants in the P2P network. There are several types of consensus, the most common of which are PoW (proof-of-work), PoS (proof-of-stake), DPoS (delegated proof-of-stake), and PoA (proof-of-authority).

Every time you create a new block, cryptocurrency is created and used as a reward and incentive for blockchain participants participating in the consensus mechanism and closing blocks, i.e., allocating their processing power, coin stakes, and other resources to support blockchain transparency and trust to verify new blocks. People created Bitcoin with this goal in mind.

Learn more: What is Blockchain – explained for beginners

Cryptocurrency holders can move cryptocurrency assets between wallets and blockchain addresses, exchange them for fiat currency, and engage in cryptocurrency trading. Everyone on the network can see transactions, but the people’s identities behind these public addresses remain hidden because they are encrypted with unique keys that link an individual to an account.

What is the Difference between Coins and Tokens?

Coins and tokens are the two significant subcategories of cryptocurrency. While both are cryptocurrencies, there is a distinction between a coin and a token. Understanding their fundamental concepts will assist you in determining how to create your cryptocurrency for specific business needs.

A token is a representation of something valuable, like an object or person. The defining feature between coins and tokens lies in how they can be exchanged for other tradable items: this means one token might represent five minutes worth of internet access, whereas another may only allow you three days at most! Suppose we’re talking about decentralized apps (dApps).

In that case, there won’t necessarily need to exist such restrictions as these will run self-sustainingly without relying on external sources – but people often purchase them with real-life goods just because they enjoy having tangible proof that what’s happening behind their screens has some authenticity attached too; we call these “tokens.”

As you may be aware, there are many different types of tokens in the crypto space.

Coins represent cryptocurrencies and can either serve as an investment or a utility token for use on an application/platform with specific features like access rights to content, etcetera.

In contrast, Tokens do not have any real-world applications themselves, which means they’re solely used within another system – called “smart contracts” to provide automatic execution after certain conditions arise (such: when someone buys XYZ coin, then it’ll execute something happened).

Learn more: NFT in a nutshell – Everything you need to know

The Benefits and Drawbacks of creating a Cryptocurrency

Cryptocurrencies are becoming more popular than ever before. Here’s what you need to know about their advantages and disadvantages!

Cryptocurrencies are a new and exciting way for people to send money around the world. They also have some disadvantages when it comes to ensuring security. Still, there’s no denying how helpful they can be in times like these where fiat currencies might not always work as intended or face hyperinflation due to economic uncertainty such recent events including Brexit (Brexit stands for British exit), which caused many British citizens’ Pound Sterling balances lose 50% of their total value by early 2018 making them worth only £100). Cryptos offer an alternative because without banks able to produce more coins on-demand, consumers could buy stuff from each other risk-free.

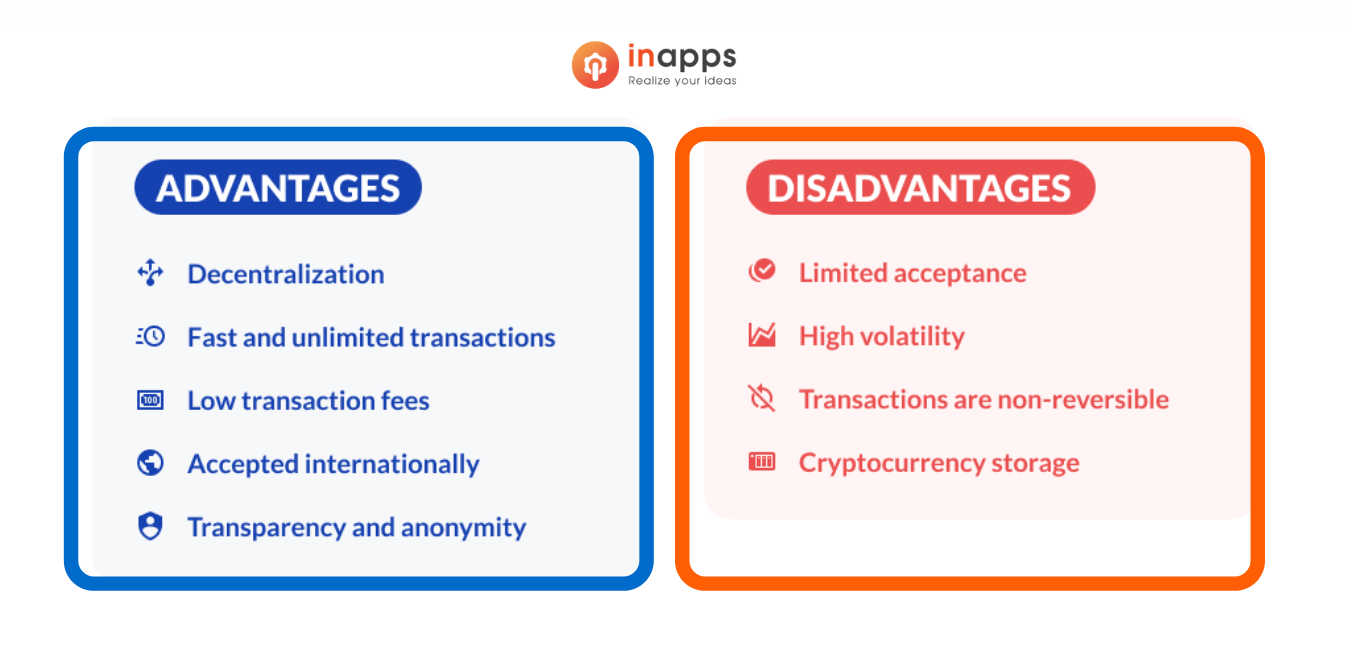

Create a cryptocurrency: Five Advantages

Decentralization

The underlying technology – blockchain – is the primary argument in favor of cryptocurrencies. This decouples cryptocurrency from any authority and ensures that no one can impose rules on cryptocurrency developers and owners.

Transactions are quick and limitless

Transactions involving fiat money take a long time to process and settle. Your company will have to wait for money for several days. With cryptocurrency, you can create an unlimited number of transactions and send them almost instantly to anyone in the world who has a crypto wallet.

Transaction fees are minimal

Banks and other financial institutions charge significant transaction fees. This is not to say that you don’t have to pay a fee for cryptocurrency transactions; however, the fee is relatively small.

Internationally recognized

The sender and receiver of funds can be located in different parts of the world and still exchange cryptocurrency. You can save money on currency conversion and the fees that are always associated with international funds transfers.

Anonymity and transparency

Because Blockchains are distributed, every transaction is recorded, and the records are resistant to change. At the same time, unless a crypto address is publicly confirmed, no one knows who made a transaction or who received the cryptocurrency.

All of the preceding should cause businesses to reconsider how to create a cryptocurrency. However, there are some disadvantages to consider.

Create a cryptocurrency: Four Disadvantages

Limited Acceptance

Countries are extremely hesitant to support any cryptocurrency. Those who want to make purchases with cryptocurrency still have few options in everyday life. As a result, rather than asking how to create a cryptocurrency, people are more likely to wonder how to use cryptocurrency at all.

High Volatility

When considering how to get started with cryptocurrency, many users overlook an important factor: high volatility. Even for well-known cryptocurrencies such as Bitcoin, the cryptocurrency market is volatile, with frequent ups and downs. Investing in cryptocurrency is extremely risky because you never know whether it will be a profitable investment or not.

Transactions cannot be reversed

Incorrectly entering a cryptocurrency address can cost you money. You can request a refund, but if it is denied, you will have to say goodbye to your money.

Storage of cryptocurrencies

You’ve probably heard horror stories about cryptocurrency owners who misplaced their devices, forgot their private keys, and were unable to access their fortunes. These kinds of situations can happen to anyone, and anyone can lose money inadvertently.

You should consider these advantages and disadvantages when deciding how to create a cryptocurrency that will help your business goals. You must determine the purpose of cryptocurrency creation for your company.

How to create a Cryptocurrency?

You can create a new cryptocurrency by either creating an entirely new Blockchain with a coin or forking an existing one and creating a token. You can find many tutorials on how to become a cryptocurrency creator on the internet, but all of them require at least basic coding skills and a thorough understanding of Blockchain.

Two ways to create a Cryptocurrency

|

Coin |

Token |

| Requires the creation of a new Blockchain | We can build it on the existing and trusted blockchains |

| Requires in-depth knowledge of blockchain and coding skills | Relatively easy to create with open source code |

| Blockchain development requires more investment | Token creation is easier, faster, and more cost-efficient |

Creating a coin

This option is not suitable if you are looking for a simple and quick way to generate your own cryptocurrency for free. You must be an experienced professional in decentralized technologies or have someone willing to assume the role of technical expert.

The process of creating a coin can take as little as 5 minutes. Simply copy the Bitcoin code, add a new variable, or change the value of something, and you have your Blockchain and coin. However, you must understand the code and how to change it, which necessitates extensive coding knowledge.

Another issue is maintaining, supporting, and promoting the coin, as you must create the entire Blockchain logic to launch your coin. Hiring a team of professionals to handle the task would save time, but would require you to pay for custom software development services. If you can afford to set aside funds for the development and maintenance of your own Blockchain, go for it.

Creating a token

This is a more practical path to becoming a currency creator. While having complete control over the Blockchain may appear to be a great idea, it comes with a number of drawbacks, including increased development time, significant expenditure, and much more.

When you build a token on top of a strong Blockchain, such as Ethereum, you’re a token that runs on a secure network that is immune to malicious attacks. Token creation is less expensive in terms of money and time because you can use the existing decentralized architecture and consensus mechanisms.

The process to create a Cryptocurrency

Before diving headfirst into cryptocurrency development, you should consider the entire process. We will walk you through the seven main steps of creating a cryptocurrency:

Step 1: Select a Consensus Mechanism

A consensus mechanism is a protocol that determines whether or not the network will consider a particular transaction. To complete a transaction, all nodes must confirm it. This is also known as “achieving consensus.” To figure out how the nodes will do this, you’ll need a mechanism.

Bitcoin’s proof-of-work was the first consensus mechanism. Another popular consensus mechanism is proof-of-stake.

Step 2: Select a Blockchain

A coin or token requires a home, and determining which blockchain environment the coin will reside in is an important step. Your level of technical expertise, level of comfort, and project objectives will all influence your decision.

Step 3: Make the Nodes

Any distributed ledger technology (DLT), including blockchains, is supported by nodes. As the creator of a cryptocurrency, you must decide how your nodes will work. Do they want a permission blockchain or a permissionless blockchain? What would the hardware specifications look like? How will hosting function?

Step 4: Construct the Blockchain Architecture

Before launching the coin, developers should be utterly confident in the blockchain’s functionality and the design of its nodes. There is no turning back once the main net is launched, and many things cannot be changed. That’s why it’s common practice to run things through telnet first. Simple things like the cryptocurrency’s address format could be included, as could more complex things like integrating the inter-blockchain communication (IBC) protocol to allow the blockchain to communicate with other blockchains.

Step 5: Integrate APIs

Application programming interfaces are not available on all platforms (APIs). Making sure a newly created cryptocurrency has APIs could help it stand out and gain adoption. Some third-party blockchain API providers can assist with this step as well.

Step 6: Create the Interface

It’s pointless to create a cryptocurrency if people find it difficult to use. Web servers and file transfer protocol (FTP) servers should be up to date, and programming on both the front and backends should take future developer updates into account.

Step 7: Legalize the Cryptocurrency

In 2017 and 2018, cryptocurrency existed in legal limbo. Depending on the circumstances, they may not have realized that creating or promoting new coins could result in fines or criminal charges. Before launching a new coin, it’s a good idea to familiarize yourself with the laws and regulations governing securities offerings and other related topics. Given the complexities of the issues and their frequent updates, you may want to consult with a lawyer who specializes in this area to help you through this step.

The Takeaway

While you can decide how to create a cryptocurrency in the best way possible, entrusting your business to an experienced software development company is more efficient.

As previously stated, you must select the right team by using the proper software vendor selection criteria to bring your idea to life. Consider hiring experienced blockchain and cryptocurrency professionals. Though the services will not be inexpensive, you will avoid the need for additional work in the future.

Make your own cryptocurrency with InApps

The cost of creating a cryptocurrency depends on the project’s specific needs and whether you choose to create a new cryptocurrency from scratch or use an existing blockchain as the underlying technology. It is entirely up to you to determine how to create a cryptocurrency.

The most difficult aspect of creating your own cryptocurrency is dealing with technical issues. You can easily find tutorials on how to create your own cryptocurrency in 15 minutes or how to create a cryptocurrency without coding, but creating a cryptocurrency is not simple. To achieve the goal, you must have extensive experience in blockchain programming. Only qualified professionals have the knowledge and experience to guide you through this difficult task.

Established in 2016, InApps Technology has continually evolved over the past years to reach the forefront of being a leading software outsourcing company in Vietnam. InApps has had experience in developing Digital Assets using Blockchain. If you are looking for a partner to deliver Blockchain solutions and consulting services, we are the right one.

Let’s create the next big thing together!

Coming together is a beginning. Keeping together is progress. Working together is success.